{kind=link}

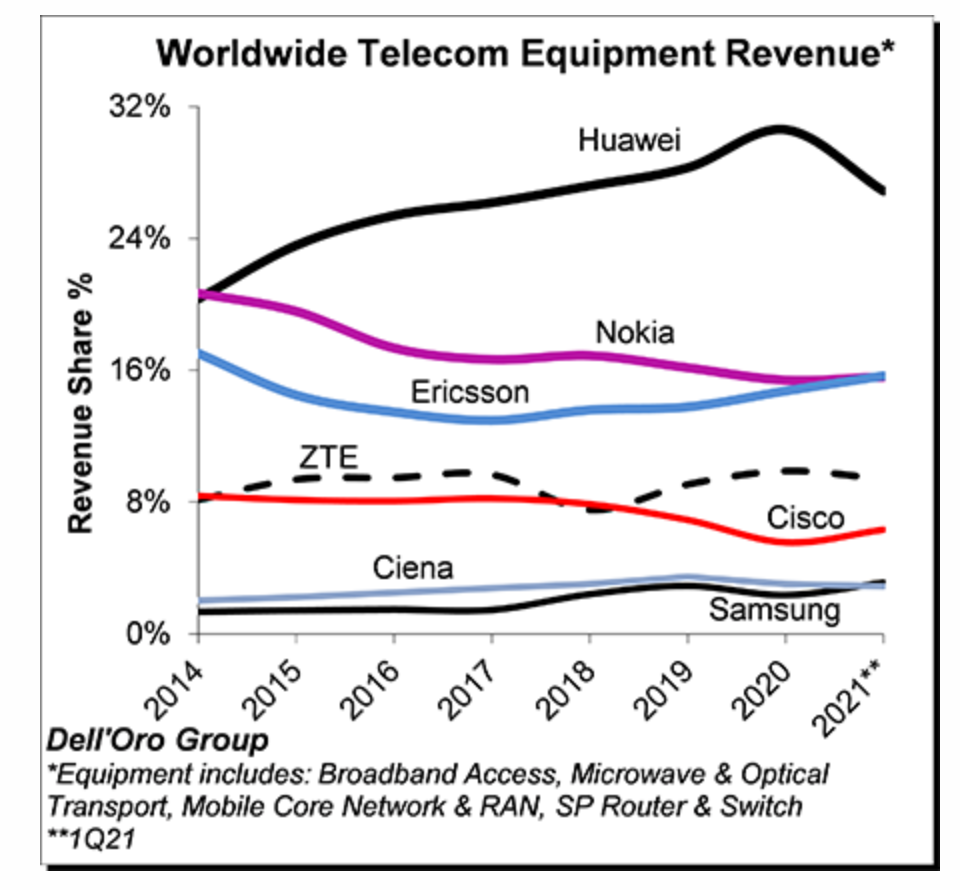

The gap between Ericsson and Nokia closes, but Huawei holds onto the top spot.

Research house Dell’Oro Group says preliminary data about the equipment market indicates its up 15% on the same period last year.

This continues the upward trend of consecutive years of growth from 2018 to 2020.

The research includes broadband access, microwave & optical transport, mobile core and RAN, service providers routers and switches.

Stefan Pongratz, analyst with Dell’Oro Group, says the rise reflects “positive activity in multiple segments and regions, lighter comparisons [ie the effects of pandemic conditions in Q1 2020], and a weaker US dollar”.

Stable places

Even so, it seems the collective global share of the leading suppliers remained relatively stable between 2020 and 1Q21, with the top seven vendors comprising about 80% of the total market.  Huawei maintained its leading position, but the gap between Nokia and Ericsson, which was about 5% points in 2015, continued to shrink and disappeared in the quarter.

Huawei maintained its leading position, but the gap between Nokia and Ericsson, which was about 5% points in 2015, continued to shrink and disappeared in the quarter.

Excluding North America, Dell’Oro estimates that Huawei’s revenue share was about 36% in the quarter, nearly the same as the combined share of Nokia, Ericsson, and ZTE.

Meanwhile, Samsung passed Ciena in the quarter to become the sixth largest supplier. This week Samsung was named as one of Vodafone Group’s principal suppliers for its Open RAN infrastructure in Europe and beyond.

Other trends suggested by the 1Q21 reporting include:

• Poor market conditions in 1Q20 as a result of supply chain disruptions impacting some segments, plus positive developments in the North America and Asia Pacific regions, helped lift and acceleration growth in the Q1 2021 compared with Q12020.

• The results in the quarter were about 2% above what Dell’Oro anticipated.

• The shift from 4G to 5G continued to accelerate “at a torrid pace”, impacting RAN investments and spurring operators to upgrade their core and transport networks.

• At a high level, the suppliers did not report any material effects from the ongoing supply chain shortages in Q1, but multiple vendors indicated the situation is less clear in the second half of this year.

Overall, the Dell’Oro analyst team is adjusting the aggregate forecast upward and now project the total telecom equipment market to advance 5% to 10% in 2021, up from 3% to 5% with the last forecast.