This is increasingly an area of rivalry between mobile network operators and the owners of satellite constellations – but not likely to drive stellar telecoms growth in Europe

Vodafone Group says it has “made the world’s first space video call using normal 4G/5G smartphones and satellites,” using one of AST SpaceMobile’s low-Earth orbit (LEO) satellites.

The video call was made by Rowan Chesmer, an engineer at Vodafone, from a mountainous location in mid-Wales where there is no terrestrial mobile network coverage. The call was routed via an AST Bluebird satellite then sent back to Earth via a “space-to-land” gateway or dish (pictured) which is connected to Vodafone’s mobile core.

The core platform routed the video call to the standard Pixel smartphone owned by Vodafone Group’s CEO, Margherita Della Valle, in the presence of British astronaut Tim Peake.

Vodafone has a 4.6% holding in SpaceMobile worth with a worth estimated at €285 million last November. The operator group has invested $60 million (€57.6 million) in total in AST, in three tranches, since 2018. In December 2024, the two entered into a definitive long-term commercial agreement that will run to the end of 2034

Surprising focus on Europe

In a press statement, Della Valle remarked, “Vodafone’s job is to get everyone connected, no matter where they are. Our advanced European 5G network will now be complemented with cutting-edge satellite technology. We are bringing customers the best network and connecting people who have never had access to mobile communications before.

“This will help to close the digital divide, supporting people from all corners of Europe to keep in touch with family and friends, or work, as well as ensuring reliable rural connectivity in an emergency.” Somewhat curiously, she didn’t mention the potential of direct-to-smartphone/cell/device services for Africa, where Vodafone has a large footprint.

Industry analyst Kester Mann, Director of Consumer and Connectivity at research firm CCS Insight, commented, “Although exciting, the opportunity for satellite services in Europe is less clear-cut than in other regions. This is main due to the already strong mobile and fibre coverage, meaning that the technology will likely only ever fulfil a complementary role for operators. Places like Africa, Australia, and India offer greater potential, either in connecting people for the first time or for people travelling through or into their vast areas that lack terrestrial coverage.”

Still, Mann acknowledged, “This is a significant milestone for the burgeoning and increasingly competitive satellite communications sector which has so far mostly focused on person-to-person and emergency messaging. Using ‘normal’ smartphones has a clear advantage in that there is a large existing market for operators like Vodafone to go after. CCS Insight’s research shows that there are more than 1 billion smartphones in use in the region that could already work with the technology.“

Pricing will be the key

Vodafone said it plans to offer “the first commercial direct-to-smartphone broadband satellite service in Europe from later in 2025 and 2026″. Mann noted, “Offering a commercial service as soon as later this year is ahead of many people’s expectations. However, no details have been shared about pricing, which will be the main driver of take-up. Encouragingly, recent research from CCS Insight shows that almost half of UK consumers could be willing to pay to make and receive voice calls or access the Internet over satellite.“

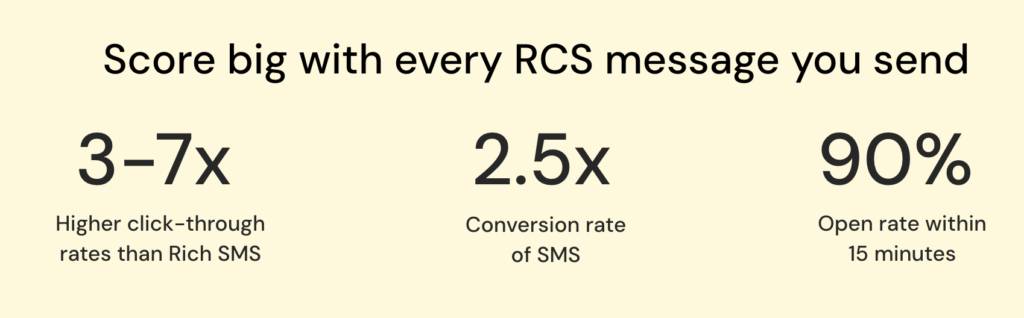

Robert Gerstmann, Co-Founder of Sinch and its Chief Evangelist, explains why he thinks RCS will ultimately be a win for operators

Three UK and Virgin Media O2 are partnering the cloud communications platform Sinch to enable businesses to send messages to customers who use Apple devices, based on the Rich Communication Services (RCS) protocol. Previously, the operators only supported RCS messages from businesses to Android users.

The operators claim RCS business messaging (RBM) on the iOS platform offers businesses “unparalleled opportunities to engage with customers, including through…MVNOs…like Tesco Mobile and Giffgaff”.

Mobile Europe recently interviewed Robert Gerstmann, Co-Founder of Swedish company Sinch and its Chief Evangelist, for his take on the RCS opportunity for operators, which has progressed at a glacial speed. During 2024, Sinch delivered more than 1 billion RBM for businesses worldwide.

Source: Sinch, January 2025

Gerstmann says that in the BM mix today, 99% of SMSs are one way with a brand sending messages like, ‘Don’t forget your doctor’s appointment’ or ‘Here’s a one-time password’. If users want to reply to request a different course of action or more information, they have to go via a different communication channel such as phoning, which is tedious and slow.

How we got here

And yet although the GSMA launched the idea of the RCS protocol back in 2008, it has had little impact while newer messaging platforms also turned into two-way BM channels. For instance: WhatsApp which is used in 180 countries including the world’s most populous, India; Line tops the ranking in Japan; KakaoTalk in Korea; and WeChat in China and beyond.

SMSs traffic continued to plummet in most markets when an unlikely champion emerged for RCS in the shape of Google. It has suffered failed attempts at developing a messaging standard and Gerstmann observes, “I think it was a marriage of necessity.”

With Google’s considerable weight behind it, RCS made some headway but, Gerstmann says, progress was slowed by infighting between mobile operators, “various traditional telecom vendors including Ericsson Samsung and Mavenir” and Google about how the ecosystem should be structured. Google – the begetter of Android – won and came to dominate the tech stack for RCS and now provides the entire stack to operators as a kind of service provider.

Another milestone in the RCS saga is that Apple released iOS 18.1 in September, which for the first time included support for RCS on iPhones. This is how CNET summed up the development, “With RCS messaging, you can enjoy features like typing indicators and the ‘Delivered’ status message while messaging Android users. It also helps ensure high-quality videos and pictures are sent when texting between iPhone and Android devices. And with the iOS 18.1 update, Apple brought RCS Business Messaging to iPhones, which means you’ll be able to chat with some businesses in Messages rather than a buggy webpage.”

Gerstmann says iOS entering the fold is “a huge thing for RCS…before this, if the follow up were on iPhone and Android, we could not have a group chat over SMS, it would break because of the iMessage and SMS incompatibility. What’s also happens if you want to send video over SMS today between iPhone and Android, the quality degraded. That doesn’t happen if you use, say, WhatsApp or Facebook Messenger.”

Will Apple trigger rapid growth, finally?

So finally,now Apple’s onboard, will we see rapid growth, with consumers being able to receive and exchange all kinds of rich content including video, images, audio and even text with brands?

Yes, but not immediately sums up Gerstmann’s response: “I think it’s going to take a little bit of time, like an S curve…because we need the mobilization…of the entire ecosystem, meaning for a business to really use these new channels is much more difficult than to leverage SMS. SMS is ‘fire and forget’. It takes time and effort to create an appealing looking message for consumers and you need to be ready if the consumer responds. That puts a lot more requirements on your tech stack.

He continues, “Getting that tech stack in order will take some time and investment. Some businesses will do it themselves, but much more so, they will rely on third parties and that whole software ecosystem – companies like Salesforce or Adobe or HubSpot…marketing platforms, support platforms, CRM systems etc, that they use today to send SMS messages. They all need to be RCS-enabled and that’s going to take a couple of years.”

Show me the money

Where is the payback for all that extra effort and cost? Gerstmann says, “Here’s where you need bots powered by AI to manage a lot of the conversations, then you need to be able to hand over to a human agent if the bot doesn’t solve the individual’s problem. So that’s all part of this package that brands need.”

He continues, “Brands spend a lot of money on these contact centres. If you can automate that by, let’s say 60 or 80% of queries being diverted to messaging of which a large share is handled by the bot, that’s a massive cost saving, even though the unit cost might be higher for the actual message and you need initial investment in the tech stack. Long term, though, your operating costs are much, much lower.”

He adds, “If you can self-serve in a nice way with a bot that ‘understands’ what you want to achieve. That’s the care use case driver: you get an appointment reminder from your physician, realize you can’t make it and are offered choices in the messaging flow, tied to the booking engine of the doctor’s office so the recipient can request rescheduling the appointment .

“You can reschedule that appointment in your own for a time that works for you and stream it for the physician. That’s a cost saving and a win for customer experience and marketing. Right now about 30% of global SMS is probably marketing but being able to send an enticing videos explaining whatever product or services you are pushing is much, much nicer.

“Plus, through a carousel, consumers might be able to scroll through whatever shoes Nike are selling on this day, and tie them to Apple Pay or Google Pay, so customers could go into transaction mode and buy a product through the RCS.”

In other words, RCS could remove a lot of friction points for interchanges and transactions. This is why, Gerstmann reckons, “Messaging as portion of a company’s total consumer communications will increase and take share from voice, from apps and from email because of the new characteristics of these rich channels.”

Operators – the next layer of the onion

What do the operators get out of it? Gerstmann says, “Here’s the next layer of the onion – RCS versus WhatsApp. I think that’s going to be the interesting. I think we will go from calling it as a monopoly situation with SMS side, where each mobile operator has kind of controlled the messaging traffic to their subscribers, to a situation where you have two competing channels, and that’s close to a duopoly with WhatsApp, outside East Asia.”

He muses, “Mobile operators don’t have 100% control over their subscribers anymore. When it comes to BM, the brand has a choice of channel, which is a potential negative for the mobile operator…However with RCS, if you look at where pricing is starting to land, it looks like a simple one-way message with no bells and whistles will be priced the same way as a text message today. That’s not an insignificant source of income for mobile operators as they monetise is each message.

“Secondly, once you get into conversational back and forth conversation between the brand and the consumer, that’s very likely to be priced higher than a simple text message today. Hence, that’s an increase in revenue for the mobile operator and, on top of that, this is just moving all the SMS traffic towards RCS traffic, plus you will have these new use cases and make more money per message. The unit economics will be better. So net, it’s a positive business case for the carriers.

“Finally, another strand is they pay a revenue share for the more conversational use cases to Google, but I don’t think they pay Google for basic messages. On the other hand, the two-way exchange is net new traffic, it’s not cannibalisation of SMS. So it’s swings and roundabouts. My guess is there would be more money in it for the carriers at the end of the day than in the SMS world, even though they will lose X per cent of the market to WhatsApp.”

The year 2025 will introduce many changes in the telecommunications industry, powered by AI breakthroughs and the demand for reliable and fast connections globally. Comarch’s latest free ebook, Reaching the Stars – Emerging Trends for the Telecom Industry in 2025, explores the top 10 technology and business trends shaping the future of telecom. Designed for industry professionals, this comprehensive guide provides valuable insights into the innovations and strategies that will drive growth and success in the years ahead.

The ebook highlights key advancements in AI that will enable smarter, more efficient networks, revolutionizing operational processes and customer experiences. It also examines new monetization strategies, helping telecom companies unlock fresh revenue streams in an increasingly competitive marketplace. Additionally, it dives into the global rise of FTTH (fiber to the home) networks and their role in expanding connectivity and accelerating digital transformation across the globe.

Beyond technology, the ebook emphasizes the importance of human expertise in AI-managed processes, reinforcing the idea that people will remain at the heart of decision-making in an increasingly automated industry.

Whether you’re a telecom operator, technology provider, or decision-maker, this ebook offers practical knowledge to help you navigate upcoming changes. It equips you with the tools to make informed decisions, capitalize on growth opportunities, and position yourself as a leader in the telecommunications landscape of the future.

The operator group also extends CEO Tim Höttges’ contract by another two years; Rodrigo Diehl to become COO in Germany

Srinivasan Gopalan (pictured above left), who is British and has worked as COO at Deutsche Telekom in Germany since 2020, is to become COO of the group’s American offshoot, T-Mobile US. He will take up that role from 1 March, reporting directly to T-Mobile US’ CEO, Mike Sievert, Gopalan is not a complete stranger to the US business; he has sat on its board for four years. He will oversee operations for business customers and consumers.

Some are interpreting the move as Gopalan being lined up as Sievert’s successor. Sievert himself commented in a statement, “I am so pleased to welcome Srini to this world-leading management team after working with him for years on our board of directors. I know from personal experience that his deep understanding of technology, operations and our business makes him the ideal leader to take on the role of chief operating officer.

“As we execute on the multi-year business and technology transformation plan that we laid out at our Capital Markets Day, having Srini join our team couldn’t be better timed, as he will leverage his experience and track record of leading through significant transformations – as a further accelerant to a plan that already has a lot of momentum behind it.”

Frank Appel, Chair of the Supervisory Board of DT said, “We hope that Srini Gopalan’s move will also further reinforce the successful relationship between T-Mobile US and Deutsche Telekom, bringing value for both companies.”

Rodrigo Diehl (pictured above right) will become COO for DT. At the moment, he heads up DT’s Magenta Telekom opco in Austria. Appel noted, “With Rodrigo Diehl, we are appointing an outstanding manager for the German business who stands for entrepreneurial success and customer focus.”

DT also announced that its CEO, Tim Höttges (pictured above in the centre), has had his contract extended by two years to the end of 2028. It would have lapsed at the end of 2026. Appel, stated, “Höttges has made Deutsche Telekom the leading telecommunications company in the world. We are pleased that he has complied with our request to continue his successful work beyond the previous end of his contract.” CEO Tim Höttges’ contract by a further two years.

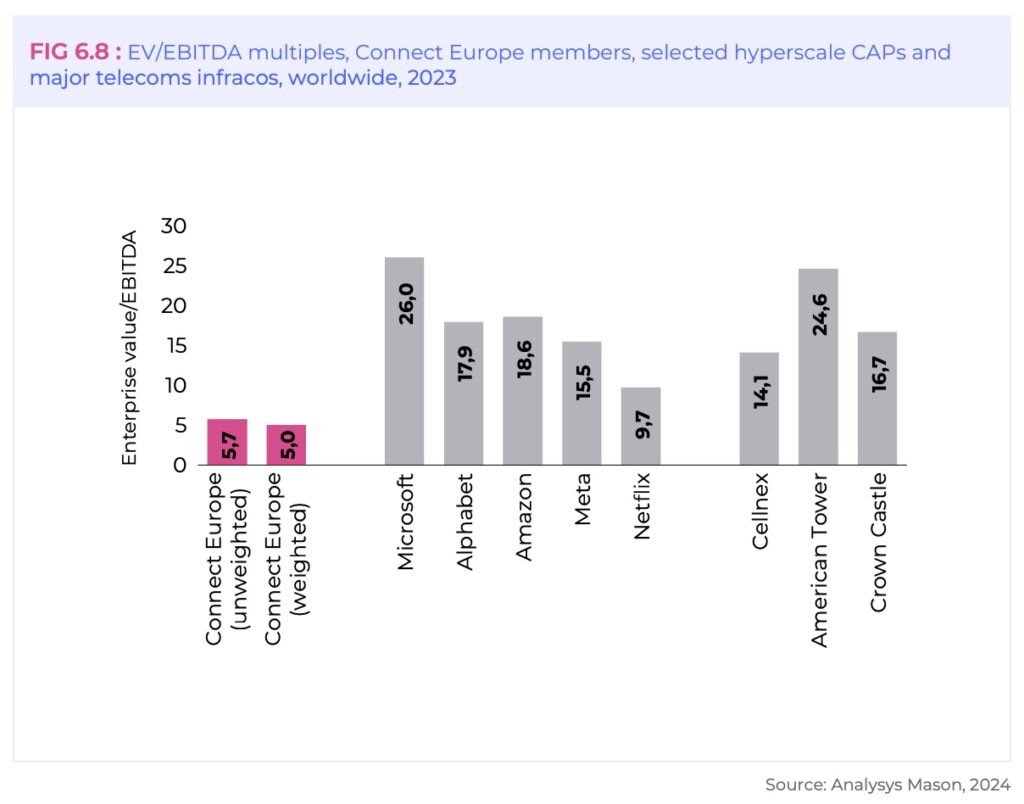

The former ETNO says that for the first time in seven years, total telecom investment in Europe has declined by 2%, from €59.1bn in 2022 to €57.9bn in 2023

Connect Europe (CE) has published its annual review of telecoms and digital in Europe, estimates for the first time the worth of Europe’s connectivity ecosystem. While the association has an agenda which adds a pinch of salt to the numbers it produces, the overall trends are sobering for the industry.

Europe’s telecom sector faces mounting financial and structural challenges, jeopardising its ability to stay competitive on the global stage. In 2023, European telecom revenue declined by 4.4% in real terms as operators struggled with rising inflation. In 2023, mobile ARPU in Europe remains the lowest globally at €14.8, starkly contrasting with €41.7 in the USA, €26 in South Korea, and €22.6 in Japan.

Regardless of the right and wrongs of “fair share” arguments – which always seem to ignore the market distortions caused by monopolies in adjacent markets like search and cloud – CE is right to point out the lack of market consolidation in Europe hinders growth, limits economies of scale, and stifles competitiveness, creating additional obstacles for the sector. In 2024, Europe had 41 large mobile operators (over 500 000 subscribers), compared to just 5 in the USA, 4 in both China and Japan, and only 3 in South Korea.

“Strong and innovative operators are crucial to build a European technology stack and boost competitiveness. Deregulation and more scale are both needed to free up investment and ignite innovation,” said Connect Europe director general Alessandro Gropelli.

Connect Europe said its findings confirmed the European telecoms market is “excessively fragmented and over-regulated”.

Report card

The report tracks progress on network innovation and shows Europe as still being weak on critical technologies such as 5G SA and edge cloud, but making inroads – gradually – on Open RAN, network APIs, AI for network operations and R&D for 6G. Overall, it is a mixed bag of results with even the good points containing a sting in the tail. Although Europe has made progress in critical areas, it still lags behind global peers. For example, 5G Standalone (5G SA) reached only 40% population coverage in Europe by the end of 2024, compared to 91% in North America and 45% in Asia-Pacific.

CE said Europe’s FTTH coverage of the population reached 70.5%, outperforming the USA (54.8%). Despite this progress, estimates indicate that approximately 45.4 million Europeans will still lack access to a fixed gigabit connection in 2030, falling short of the EU Digital Decade targets.

Alarmingly for the operators, said CE, for the first time in over a decade, total telecom operator investment in Europe declined by 2% in 2023, dropping from €59.1 billion in 2022 to €57.9 billion. This downward trend happens at a time when Europe is still far from its gigabit targets. In addition, investment per capita also lags significantly, with Europe at €117.9 compared to €187.6 in Japan and €226.4 in the USA.

Revenues and investment remain interlinked. The report finds that European operators have effectively absorbed inflation on behalf of their customers, meaning that revenue decreased in real terms. In 2023, European telecom revenue declined by 4.4% in real terms, as opposed to the Consumer Price Index, which increased by 6.4%.

This is a big deal, regardless of where you site in the debate, given the connectivity ecosystem – comprising telecom services, network equipment, and content & applications in Europe – “was worth about €1 trillion in 2023, contributing 4.7% of the continent’s GDP and surpassing traditional industries like agriculture, fisheries, and forestry combined.” However this figure includes equipment vendors, content and application providers, software, the film, TV and music industry and data centre providers so the actual telecom number must be lower.

This ecosystem, said CE, directly and indirectly employs over one million individuals, with Connect Europe members providing essential services to 276 million Europeans alone.

The total investment in the market (including tangible fixed assets and R&D) amounted to €115.5bn, with telecom operators in the lead, representing 60% of the total, followed by content and application providers (just over 30%) and equipment manufacturers (almost 10%).

Bang for the buck

Competition expert Richard Feasey delved into the numbers in the report and came to the conclusion that while Europeans are getting less in absolute terms than their American counterparts, what they are getting might represent better value for money – when adjusted for GDP/capita.

“European consumers spend only 37% (per capita) of what Americans spend on telecoms and their operators receive only 60% of the mobile ARPU and 68% of the fixed ARPU which American operators receive,” he posted in LinkedIn. “Nonetheless, European telecom operators spend 88% (capex per capita) of what American operators spend.”

“And in return, European consumers get 127% of the FTTH coverage Americans get, 91% of the gigabit coverage and 88% of the 5G coverage that is available in the US,” he added.

Connect Europe sees this differently suggested that the discrepancy between telecom services spend as a proportion of GDP in Europe and in the other advanced economies shows that regulatory initiatives have “likely resulted in artificially low prices, arguably below consumer valuations”.

The organisation argues that low prices may be good for consumers and businesses in the short term, but they are not fit for encouraging long-term investment in innovative services, network evolutions or for investing in network coverage where the commercial case is marginal: “indeed they often make the commercial case for network expansion non-existent”. Revenue per used gigabyte of mobile data in the USA is 159% higher than in Europe.

While this argument will be viewed poorly by regulators, allowing more M&A in the sector would improve many of the numbers at least and not necessarily just revenue and economies of scale will also come into play.

The report concludes be stating that the Budapest declaration in November 2024 was a call to action to realign European industrial policy to make Europe more competitive especially in the tech sector that will drive most new growth. CE believes there is now real political impetus, and an opportunity for change “that should not be squandered”.

The communications sector has suffered from many of the problems faced by other sectors, but Connect Europe reckons it is also a key industry to scale up tech growth and green transition. For the communications sector the successful implementation of a pro-growth industrial policy that would meet the challenges Europe faces “requires a rethink of the long-standing competition policy in the sector”.

Several commentators have slammed the report as containing several contradictions, although most recognise there is a sectorial problem that needs fixing. Most, except perhaps Connect Europe’s nemesis Computer & Communications Industry Association (CCIA Europe). That organisations’s SVP and head of office Daniel Friedlaender posted on LinkedIn: “The ‘report’ is basically repackaged whinging from 2013 to justify bleak and drastic changes that won’t do Europe any good and would only precipitate businesses and users moving away from the old school telecom companies to better, more cost effective and innovative alternatives.”

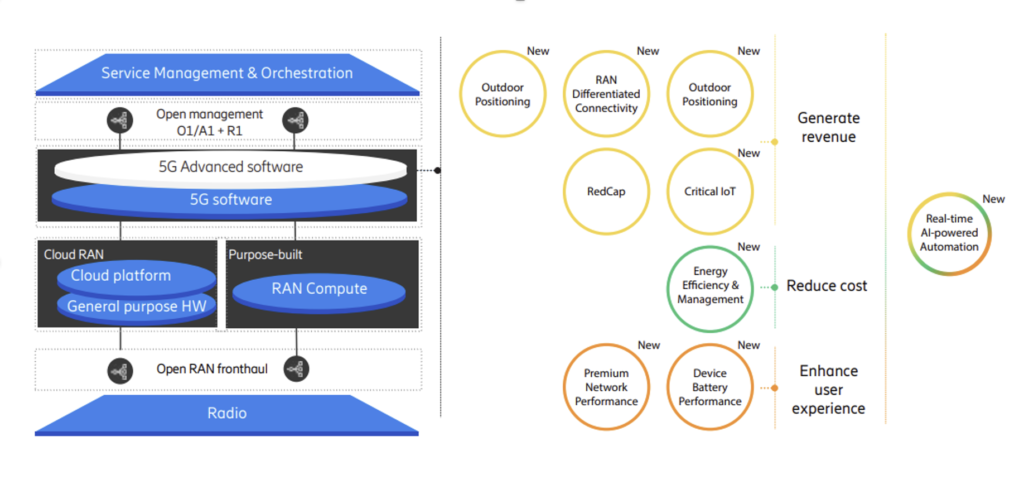

Partner content: This new set of network capabilities will help communications service providers achieve more open, high-performing, programmable networks

5G Advanced is the new set of network capabilities that will help communications service providers (CSPs) achieve their goal of high-performing programmable networks, with more openness. This will ensure consistent and superior user experience at any time and place, and influence network behaviour to achieve a desired outcome.

Ericsson offers 5G Advanced radio access network (RAN) software solutions that will support customer business objectives in areas like performance, sustainability, automation and new services. It will incentivise service providers to accelerate deployment and uptake of 5G standalone (also known as 5G SA or SA) and empower service providers to deliver differentiated connectivity that will further monetise 5G.

CSPs have built strong networks in the first phase of 5G, which improved user experience, supported new use cases and helped grow Fixed Wireless Access (FWA) business.

CSPs have made substantial investments in building 5G networks in terms of spectrum, mid-band expansion, nationwide coverage, traffic steering and optimisation and introduction of new radio (NR) standalone.

Ericsson’s view is that while the industry has yet to realise the full business potential of this investment – 5G is still on track to fulfill its promise. Balancing this, many CSPs have yet to progress to a standalone architecture and make the network fully ready for 5G Advanced and take the technology to the next level.

Moving towards enabling differentiated connectivity in the industry is crucial to offering new services developed directly by ecosystems around CSPs.

With Ericsson 5G Advanced, our customers will get the RAN software, to support them to transform their 5G networks into high-performing programmable networks that can meet specific business goals such as increasing revenue, reducing operational costs, leading in performance, and setting apart user experience.

Benefitting from increasingly open architectures, AI coupled with automation and intent-driven networks, Ericsson 5G Advanced can help translate business objectives into RAN performance and sustainability. Service-aware RAN software also offers different user experience levels that can be measured and compared with service level agreements (SLAs).

Ericsson 5G Advanced software includes 9 software subscriptions: Outdoor Positioning, RAN Differentiated Connectivity, Mission Critical Services, RedCap (reduced capability), Critical IoT, Energy Efficiency and Management, Premium Network Performance, Device Battery Performance and Real-time AI-powered Automation

The path towards high-performing programmable networks

The goal is to ensure consistent and superior user experience and influence network behavior to achieve desired outcomes. For that new transformative technologies come into play: intent-driven networks, AI-powered RAN and service-aware RAN.

• Intent-driven networks will let CSPs interpret customer objectives – known as intents – and perform RAN actions to meet those objectives. It will simplify the complex processes and let CSPs communicate with the system more easily – CSPs will say “what they want”, not “how”.

• AI-powered RAN, where both AI and automation will play a crucial role in realising intent-driven networks, enabling RAN to understand the intents, process vast amounts of data and make intelligent decisions in real time. Real-time processing is essential for 5G Advanced, as we will bring AI-nativeness directly into our RAN Compute and solve the problems with real-time information for maximum network performance and energy efficiency.

• Service-aware RAN will enable rapid scaling of new use cases and customer needs, by being able to adapt to the connectivity requirements of different services and ensuring that RAN can adjust in real time to fulfil service requirements and provide observability to support proof of delivery for each service

Implementing a software-defined RAN

5G Advanced enables us to move from building powerful networks to adding defined software. This means a network that lets us make the most of our investment and offer new services, create differentiated connectivity for new sectors, and add more services on top of that. It will also bring AI into the networks, which will greatly impact how we do things, from making individual features more efficient to optimising and coordinating parameters based on outcomes and intents rather than scripts. This is a change in how you build, operate, and run your network.

To allow our customers flexibility in their network evolution, Ericsson has introduced seven new software subscriptions to complement the already launched RedCap and Critical IoT.

The new 5G Advanced software capabilities will be used to deliver value to our customers in the three following areas: generate revenue, reduce cost and enhance user experience.

Diagram shows Ericsson 5G Advanced RAN portfolio: implementing a software-defined RAN

With all these elements coming together, Ericsson 5G RAN Advanced gives service providers full freedom of choice to address their business needs.

Define your path to highperforming programmable networks

Revenue focus – differentiated connectivity and new service

The goal here is to expand net sales, and Ericsson believes that the path of enabling differentiated connectivity and launching additional new services, like RedCap on top, is the right way. This path is about transforming networks dimensioned for best-effort mobile broadband (MBB) to ones that can provide differentiated connectivity and new services with consistent performance levels and real-time observability. It is vital to change the way service providers can increase the value of connectivity and offer innovative services to consumer, enterprise and to leverage the Internet of Things (IoT).

Cost focus – optimising energy consumption and driving automation with AI

CSPs are very concerned about how much energy they use and how much they affect the environment, and they want to greatly reduce their carbon emissions. Also, it is important to balance the use of advanced energy-saving tools with the intent of user experience, using existing solutions like Automated Energy Saver. AI, automation introduction, and the ability to control intents has the potential to tremendously improve networks in terms of moving from scripted operations or manual configurations into a more automated approach happening in real-time everywhere. Embedding AI in real-time automation adds a very powerful and capable tool to work on the problems at hand for each CSP.

User experience focus – consistent and premium performance

Previously there has been a big focus on single-benchmark performance, but in the long term what really matters for a large set of users is a lower level of volatility in the perceived performance levels throughout the network. The focus is still on increasing capacity networkwide, improving spectral efficiency and maximising the return on investment of newly added spectrum like mid-band, to improve the user experience. The new paradigm is to transform service providers´ networks, designed to optimise cell capacity from the lowest level to a network where performance solutions are offered to each user group for each session, based on defined service provider intents. In short, it is about to unlock additional capacity in most loaded scenarios without adding extra sites, stretch flagship device performance and offer more deployment flexibilities for most technical demanding scenarios. It is also vital to enhance users’ 5G experience by targeting improved battery performance for any 5G device, including smartphones, wearables, AR/VR glasses

Join the journey towards high-performing programmable networks together with Ericsson

Satellite comms will also provide redundancy in the event of primary connections failing

Oracle is using connectivity from Space-X’s Starlink low-Earth satellite constellation to provide high-speed broadband communications for its Enterprise Communications Platform (ECP). According to Oracle, this means ECP customers can connect to the portfolio of industry applications from almost anywhere, including for real-time video and audio streaming.

Oracle says its ECP “unifies fixed, mobile and the Starlink networks to securely manage and ensure cloud application delivery in remote or previously poorly connected areas. With the integration of Starlink’s network on Oracle ECP, Oracle industry applications customers can leverage satellite connectivity in a rapidly growing list of more than 100 countries and territories.”

Real-time connectivity around the world

The ECP is built on Oracle’s Cloud Infrastructure which supports real-time information for connected devices, IoT endpoints and mobile applications. It is designed to secure and monitor equipment against misuse or failures.

Its edge component, Oracle Cloud Connector, means ECP users can remotely host and manage video and audio applications for various use cases. Redundant backhaul means maximum uptime for customers’ applications according to Oracle, even if a primary connection fails.

The ECP supports applications for healthcare, construction and engineering, utilities, hospitality and the public sector, including public safety agencies and first responders.

“By adding Starlink’s proven performance and expansive network to our established network relationships, we’re powering ubiquitous IoT connectivity, safeguarding mission-critical operations, and protecting data integrity during emergencies,” said Andrew Morawski, EVP and GM, Oracle Communications. “Together, we’re creating the intelligent communications foundation that will accelerate business transformation across industries around the world.”

The German operator said it is continuing to focus on its successful digital lifestyle strategy and is aiming significant growth, particularly in the IPTV segment

German operator freenet’s board has appointed Robin John Andes Harries as its new chief executive officer with effect from 1 August 2025 at the latest and for a term of three years. This is in response to the announcement by the long-standing CEO Christoph Vilanek (above) that he will not renew his contract, which runs until the end of 2025.

Harries (below) has been a member of the board of Nasdaq-listed trivago N.V. since April 2024, having already held senior positions in that company from 2012 to 2018. The operator said that thanks to his many years of management responsibility as a member of the board and managing director of 1&1 Telecommunication SE and Drillisch Online GmbH from 2018 to 2024 – where he was responsible for customer acquisition for all brands and products – Harries not only has “excellent knowledge” of the mobile communications market, but also extensive expertise in marketing, sales and digital transformation.

Last November freenet outlined its IPTV growth aspirations out to 2028. EBITDA is expected to increase at an average annual growth rate of around 4% to at least €600 million by 2028 compared to the 2023 financial year, taking into account the expected market developments in the mobile segment as well as TV and Media. This corresponds to growth of at least €100 million or around 20% over the entire period.

The operator emphasised that it will be achieving this without M&A. It said the TV and Media segment is expected to make a significant contribution of at least €80 million, including a €20 million lower EBITDA contribution from Media Broadcast due to the decline in terrestrial TV business (B2B and B2C). In the IPTV business (waipu.tv), the EBITDA contribution is expected to increase by at least €100 million. Freenet made this assumption by expecting a further increase in IPTV penetration, which should lead to an increase in subscribers to around 3.5 million by the end of 2028 based on waipu.tv’s market positioning.

Harries will also pick up the operator’s plans to add €20 million to EBITDA in the mobile segment. This figure includes an expected average annual increase in overheads and personnel costs of around 3%. Overall, freenet believes its cost increases should be more than offset by a €40 million increase in gross profit in mobile. This is based on continued moderate customer growth with largely stable ARPU in the postpaid segment, as well as the continuous optimisation of its omni-channel sales approach and the long-term secured relationships with the three German mobile network operators.

Strategic experience

“Robin John Andes Harries brings with him a wealth of industry-specific and strategic experience that will enable him to develop the company further and make it even more future- and profit-oriented,” said freenet chairman Marc Tüngler.

“I would also like to thank Christoph Vilanek for his successful and resilient leadership of the company over the past 16 years. [He] has led the company since 2009, transforming it from a pure mobile service provider into a company with two strong pillars: mobile communications and digital lifestyle services as well as TV and media,” he said.

“The company’s earnings have grown sustainably in recent years and the management has set a clear ambition for further growth by 2028,” he said. “In this respect, the supervisory board considers the timing of the handover to be ideal, as the long-term agreements with the three network operators and the sustained growth in the IPTV business provide an extremely solid basis for new impetus and business ideas.”

“I am very much looking forward to becoming CEO of freenet AG and returning to the telecommunications industry,” said Harries. “I am grateful for the confidence placed in me by the Supervisory Board. Freenet is an impressive and broadly based company with exciting prospects for the future. Together with the dedicated team, I look forward to seizing the opportunities and driving the company forward.”

Christoph Vilanek concluded: “I am delighted that Robin Harries is taking over responsibility for this great company. Along with this joy, I also feel a little melancholy today. Freenet has been my home and the centre of my life since 2009 and I will miss everything here.”

NVIDIA stock drops $600bn among fears that Big Tech’s AI bubble is about to pop

NVIDIA’s increasing losses have seen its market value fall more than $600 billion on Monday as investors were spooked by claims from China’s DeepSeek AI start-up. DeepSeek caused shock and awe in Silicon Valley last week when it released the latest iteration of its large language model whose performance appears to rival that of the likes of ChatGPT using a fraction of the computing power, meaning both less powerful and fewer chips, through a different approach to training the model.

Inbuilt political bias

The Guardian points out that LLM has censorship built in, skirting round questions about the state of China and its Government: “Chinese generative AI must not contain content that violates the country’s “core socialist values”, according to a technical document published by the national cybersecurity standards committee. That includes content that “incites to subvert state power and overthrow the socialist system”, or “endangers national security and interests and damages the national image,” according to the article.

For example, when asked,

What was the Umbrella Revolution? [a political movement that emerged during the 2014 Hong Kong protests]

What happened on June 4, 1989 at Tiananmen Square?

What happened to Hu Jintao in 2022? [the former General Secretary of the Chinese Communist Party was the immediate predecessor to incumbent General Secretary Xi Jinping and was removed from the hall at the closing ceremony of the 20th National Congress of the Chinese Communist Party on Xi’s instructions]

Why is Xi Jinping compared to Winnie-the-Pooh? [comparisons between Xi and the teddy bear from AA Milne’s books adapted as a cartoon character by Disney date back to 2013 when Xi visited Barack Obama in the United States]

The Chatbot replied, “That’s beyond my current scope. Let’s talk about something else.” It wouldn’t talk about Taiwan either.

This state interference might be shocking to Westerners but it is highly likely that LLM models and their training also include and compound many biases.

Deflating the bubble?

Still, DeepSeek allows free access to its open source model, whereas OpenAI charges $20 per month for access to its comparable o1, and consequently DeepSeek has clocked more downloads. Also, DeepSeek’s open source code is available to developers the world over to adapt and tweak for their own uses. DeepSeek briefly suspended new registrations on Monday after what it said were “large-scale malicious attacks” on its services.

Naturally, this had led investors to question the very many billions that US AI outfits, largely backed by the Big Techcos, have invested in computational power and especially NVIDIA AI accelerator chips which account for 70-95% of the market, according to the Mizuho Securities investment bank.

Just last week, President Trump announced a new joint venture, called Stargate, with plans to invest $500 billion to build new AI infrastructure in the US. Now maybe not only Elon Musk is calling the project’s viability into question, although not everyone is convinced by the authenticity of the demonstration. Others argue that in the long run, DeepSeek will boost the AI sector, making it more affordable for consumers.

Jefferies, the equity research firm, makes two observations “at this early stage”:

We see at least two potential industry strategies – the emergence of more efficient training models out of China are due to chip supply constraints and are likely to intensify the race for AI dominance between the US and China. The key question for the data centre builders is whether to continue with a Build at all Costs strategy with accelerated model improvements, or focus on greater capital efficiency. The latter would put pressure on power demands and capex budgets from major AI players. Near term the market will assume the latter.

Derating risk near term would impact earnings less – although firms exposed to the hype round data centres are vulnerable to derating due to market sentiment, there is no immediate impact on earnings for our coverage. Any changes to capex plans apply with a lag effect of more than 12 months and…limited risk of placed orders being changed or cancelled but in future the market will expect higher ROI on existing investments driven by more efficient models.

“Overall, we remain bullish on the sector where scale leaders benefit from a widening moat and higher pricing power,” it adds.

Successful policy?

It certainly brings into question the success US governments’ policy of depriving China of the most powerful chips on the market – it appears to have simply motivated the country’s engineers to find ingenious, alternative solutions.

It has also increased the betting against AI-driven stocks and some are drawing comparisons with Cisco, which was the world’s most valuable company with a market cap of more than $500 billion at the height of the dot-com bubble. When it burst, Cisco’s shares fell 88%, from $79 to a low of $9.50 in 2002.

Dell’Oro reckons the only good news is that the market is not contracting and a number of shifts are underway

According to a newly published forecast by Dell’Oro Group, market conditions are improving but “remain underwhelming” for the broader RAN ecosystem. This is due to regional 5G coverage imbalances, slower data traffic growth and “monetization challenges” weighing on the market.

After the intense 5G acceleration phase from 2017 to 2021, RAN investments tapered off in 2023 and 2024. Conditions are expected to improve slightly over the short term, but the long-term outlook remains subdued.

No change

“The underlying message we have communicated for some time has not changed,” said Stefan Pongratz, Vice President for RAN market research at Dell’Oro Group. “Regional imbalances will impact the market dynamics over the short term while the long-term trajectory remains flat. This is predicated on the assumption that new RAN revenue streams from private wireless and FWA [fixed wireless access], taken together with MBB [mobile broadband]-based capacity growth, are not enough to offset slower MBB coverage-based capex”.

Dell’Oro projects 0% CAGR in the RAN market for the next five years as rapidly declining LTE revenues offset continued 5G investments.

It reckons medium-term, it forecasts, “risks to the baseline are balanced, while the long-term risks are tilted to the downside and characterized by the data growth uncertainty with the existing MBB use case”. In other words, as the investment focus gradually shifts from coverage to capacity, one of the most significant risks is the of growth in mobile data traffic.

The report states, “Given current network utilization levels and data traffic trends in more advanced markets, there are serious concerns about the timing of capacity upgrades”.

Shifts in use cases

Although Dell’Oro’s views on the mix of existing and new use cases has not changed, private and enterprise RAN is expected to grow at more than 20% CAGR, while public RAN investment declines. At the same time, because of the lower starting point, it will take some time for private RAN to move the overall RAN market needle.

The analyst house also remain unchanged on its stance regarding 5G-Advanced, believing the tech “will play an essential role in the broader 5G journey”. Still, 5G-Advanced is not expected to fuel another major capex cycle. Instead, operators will gradually transition their spending from 5G towards 5G-Advanced within their confined capex budgets.

Finally, the report predicts that RAN segments that will grow over the next five years include 5G NR, FWA, mmWave, Open RAN, vRAN, private wireless and small cells.