Communications ministry makes claim as Ifriqiya submarine cable branch pronounced ready for service after landing last month

A government spokesperson said Tunisia has identified a need for around 6 or 7 submarine cables and the country has invited operators to invest in making this a reality. The chief of staff of the minister of communication technologies Kamel Saadaoui made the claim to local news agency TAP at the ready for service ceremony for the Ifriqiya submarine cable.

Ifriqiya, which has a capacity up to 3Tbps, is connected to the main route between Marseille in France and Abu Talaat in Egypt over a 950km length from the Bizerte connection point. It is part of PCCW’s 15,000km Peace subsea cable, built by Huawei, which links Marseilles in France to Egypt and on to Pakistan, Kenya in 2022 and Singapore last year. The cable has a capacity of up to 96Tbps for the Pakistan-Egypt segment and 192Tbps for the Mediterranean segment from Egypt to France.

Ifriqiya landed at the Ain Meriem area of Bizerte, which is also currently the landing point for the SeaMeWe-4 cable. A branch of the Medusa cable is also set to land there (via Marseilles) with Orange as the partner. Tunisia’s other landing point is in Kelibia, which hosts the Didon cable (owned by Orange and Ooredoo), Hannibal, and Trapani-Kelibia cable systems.

Saadaoui said Ifriqiya was part of the nation’s strategy and represents one of the priorities in the development of the basic infrastructure of telecommunications networks, as well as an ideal infrastructure for the launch of 5G services.

Ooredoo Tunisia CEO, Mansour Rachid El-Khater, said that the Ifriqiya project is one of the strategic projects launched by Ooredoo to connect the northern Tunisian coast from the city of Bizerte to the city of Marseille in France “in record time”.

The UKA Group specialises in renewable energy and has access to a secure, regulation-compliant, cloud-based tool for Generative AI

Deutsche Telekom (DT) has signed up its first Business GPT customer, the UKA Group. The company specialises in renewal energy projects and now has access to generative AI-enabled (GenAI) tool.

Details of how UKA plans to use the tool are not specific: “With this solution, UKA offers its employees an application for everyday use and can also test innovative use cases within its specialist departments. In future, it will be possible to connect company applications directly via programming interfaces.”

Business GPT is browser based and UKA’s employees can access it via their own intranet. According to DT, “This greatly shortens the path from business case to productive usage”.

The tool is multilingual and so useful for international organisations like UKA.

DT runs the tool on secure cloud environments in Europe, so companies can use the GPT 3.5 and GPT 4.0 models from Microsoft Azure OpenAI Services in a shielded area.

The product was originally developed for use by DT’s employees, with security, data protection and employee representation built in. After successful internal implementation, Telekom MMS added Business GPT to its portfolio.

Real innovation through AI

Christian Schmidt, Head of IT and Digital at UKA, commented, “Business GPT makes us absolute pioneers. With this tool, we enable our employees worldwide to test use cases for AI language models in a secure environment and use them profitably. That’s what I call real innovation.”

“Compliance and security – that’s what our customers expect from us. It’s in our DNA,” says Klaus Werner, Managing Director for Business Customers at Telekom Deutschland GmbH. “Business GPT combines Telekom’s reliability with the latest in natural language processing and all the innovation that comes with it.”

Orange money and network upgrades to 4G are both boosting subscriber numbers as well

Sonatel, which trades as Orange in Senegal through that company’s controlling stake, has launched commercial 5G pilot to provide fixed and mobile internet to residential and business customers in the country. The operator has invited prospective customers to see 5G in action at the Orange Digital Center (ODC) in Dakar.

The launch of commercial 5G by Sonatel comes around seven months after the operator acquired the first 5G operating licence in Senegal from the Telecommunications and Postal Regulatory Authority (ARTP) for $57 million. It’s taken a while given the operator first mooted 5G in 2020 and then announced a successful test in December 2021. In July 2022, it launched the 5G ODC.

According to Ecofin, In the 5G segment, Sonatel is ahead of its main competitors Expresso Sénégal and Saga Africa Holding Limited (Free). The latter acquired its operating licence in December 2023 for CFA 13.5 billion.

According to ARTP data, Orange had 12.5 million mobile subscribers in the third quarter of 2023 for a market share of 56.47%. Expresso and Free respectively controlled 16.8% and 23.89% of the national mobile telephone subscriber base. In the Internet segment, Orange held a market share of 66.52%.

Last month, the Sonatel Group, which operates in 5 countries (Senegal, Mali, Guinea, Guinea Bissau and Sierra Leone) posted strong FY2023 results on the back of high-speed data, mobile and Orange Money. Its fixed, mobile and internet customer base increased by 6% compared to 2022 and reached 41.1 million thanks to growth in all countries and mainly in Guinea, Senegal, and Mali.

The number of active mobile data customers of the Group now stands at 19.1 million, an increase of 10.1% YoY. The active 4G base reached 14.4 million customers, an increase of 35.5 % compared to 2022. Sonatel wants to offer full 4G mobile networks in all its countries of presence – it is already doing so in Senegal and Mali.

The Orange Money customer base reached 31.6 million customers, an increase of 19.8% compared to 2022 thanks to the diversification of the portfolio of offers and the price adjustments carried out in several countries.

Sonatel’s fixed broadband customer base has 741,000 customers, including 659,000 fibre and Flybox (4G router) customers, an increase of 25.1%. Also, from CFA 15,000 per month, households can subscribe to optical fibre with 710,000 optical fibre sockets deployed by the end of 2023, mainly in Senegal and Mali.

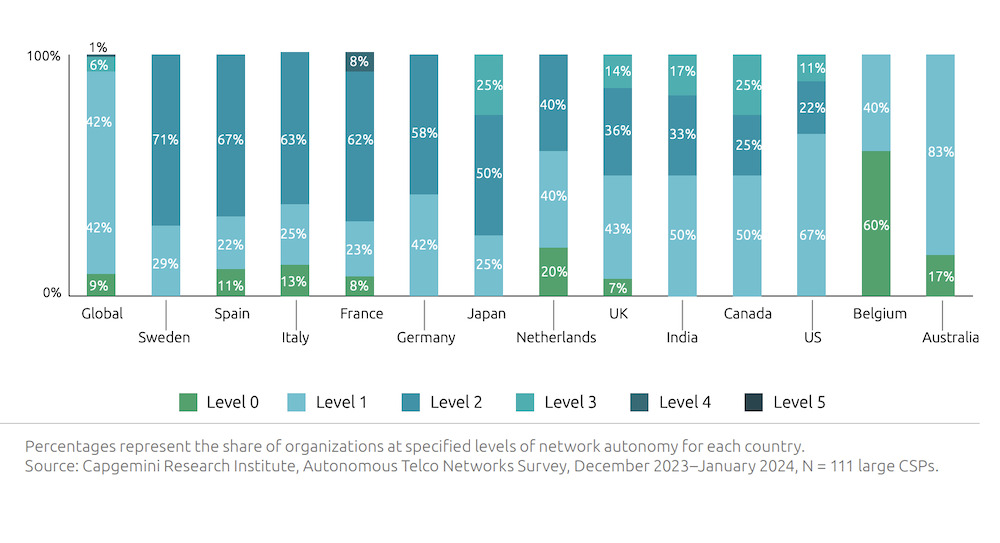

More than 60% of telcos aim to reach Level 3 autonomy by 2028 and yet only one in five has a comprehensive strategy in place

While most telcos (84%) currently reside at Level 1 or Level 2 autonomy as per the TMF definition – for their overall networks, aspirations for higher levels of automation remain optimistic. More than 60% of operatorsU aim to reach Level 3 autonomy or higher by 2028. Level 3 means the system can sense real-time environmental changes, and, in certain network domains, optimise and adjust its operation to the external environment to enable intent-based closed-loop management.

However, the path to full autonomy is fraught with challenges, both technological and organisational. Only 1% expect to attain Level 5 [full autonomy] and 16% to attain Level 4 overall (including operations). Telcos aiming to reach Level 4 and 5 believe technology will mature in the next five years, as more autonomous network use cases are implemented across network domains.

“We have a three-year and a fiveyear network-transformation plan to have an intelligent network that’s intent-based, using AI/ML. The design aims to minimize build and run cost per bit to mitigate traffic growth and the rise in input costs, in particular labour and energy. We aim to reach Level 4 in five years,” said Virgin Media O2 director of network strategy and engineering Paul Kells.

“Our ambition to reach Level 4 network autonomy (for some workloads as of 2025) plays a crucial role in the Group’s strategic plan – ‘Lead the future’ which was announced in February 2023. Through enhanced use of data and AI at Level 4 autonomy, our network will be, more agile, more effective, more resilient, and higher performing,” said Laurent Leboucher, CTO at Orange and SVP of Orange Innovation Networks.

Nearly two-thirds of telcos in Sweden, Spain, Italy, and France have attained Level 2 autonomy. One-third of telcos (33%) in the US have moved to either Level 2 or Level 3 autonomy.

Despite these – and other – challenges, there is no denying that autonomous networks offer significant benefits to telcos. Over the past two years, operators have already realised a 20% improvement in operational efficiency and an 18% reduction in network opex through autonomous networks initiatives. Additionally, 71% of operators have reduced energy consumption during this period, while they expect to lower greenhouse gas emissions by 30% over the next five years.

According to the report, telcos anticipate investing an average of $87m in autonomous networks over the next five years, with estimated opex savings for a mid-sized telco of $150m-300m per organisation during this period. Furthermore, the return on investment (ROI) of autonomous networks initiatives ranges from 1.7x to 3.4x, with a payback period of between 2.9 to 1.5 years in conservative and optimistic scenarios, respectively.

Where’s the plan?

Capgemini found that only 17% of telcos adopt a comprehensive autonomous network transformation strategy, complete with well-defined goals and target timelines. Over half (51%) of operators have a roadmap that covers only the next one to two years, leaving them with limited visibility into the future.

Such a strategy also needs a leader but only 15% of organizations have already made this appointment, while a further 31% are in the process of finding the right person.

But autonomous network implementation is a complex, systematic transformation involving many ecosystem partners and implementing solutions across different layers is challenging. Respondents suggested employee mindsets and behaviour are as big a problem as technology integration. Possibly because employees can see the writing on the wall.

A recent Harvard study found that willingness to support enterprise change collapsed to just 43% in 2022, compared with 74% in 2016. In 2022, the average employee experienced 10 planned enterprise changes – such as a restructure to achieve efficiencies, a culture transformation to unlock new ways of working, or the replacement of a legacy tech system – up from two in 2016.

“To transform to Level 4 network autonomy, it’s not only us who have to change. Our ecosystem, including vendors, system integrators, hyperscalers, and software providers, will have to reskill or upskill people to drive this change forward,” said Juan Luis Mulas, head of telco cloud, OSS and automation at Orange Spain.

Large organizations must also grapple with their legacy systems. Significant capital investment and employee training are required to switch over to new autonomous infrastructure. Hence, Capgemini also saw CSPs initially focusing on automating their existing procedures, rather than overhauling entire operations.

What do autonomous leaders look like?

Capgemini found the telcos operating at Levels 2–3 have reported notable reductions in operational costs, faster time-to-market for new services, and increased overall efficiency. Telcos with partial or conditional autonomy (Level 2–3), utilizing data, AI capabilities, and real-time insights to enable intent-based closed-loop management in certain network domains, have achieved an 11% improvement on average in operational efficiency.

Conversely, those with no or minimal autonomy (Level 0–1) have realized a modest 4% improvement on average in operational efficiency. Likewise, telcos with higher network autonomy are also saving more, with 16% reduction on average in network opex.

“We also analyzed the potential savings from reduced network opex for telcos over the next 5 years as they progress each level of network autonomy. With each advancement, significant savings are anticipated at high ROI. Telcos planning to move from Level 1 to Level 2 within the next five years expect an average savings of about $202 million at an ROI of 2x, while those transitioning to Level 3 anticipate an additional $203 million in savings. Further progression to Level 4 is estimated to bring an additional $300 million in total savings at an ROI of 4x, revealing that gains gather speed as telcos move to Level 4.

Most telcos (60%) prefer to lead the transformation of the network core themselves, but are much more open to their partners’ leading the transformation of other domains – hyperscalers in transport (53%) and hyperscalers (43%), and software vendors (49%) in services.

Head of autonomous networks, Juan Manue Caro, outlined Telefónica’s priorities for its transformation: “We’re fairly advanced in terms of autonomous use cases for transport, followed by RAN. And Assurance is by far the process where we have advanced more until now. For Core, we have just implemented the first AI closed loop use case, although we are being cautious with the level of autonomy there. It is important to gain trust before going farther due to the high impact of any potential problem of this domain.”

The report is based on the findings of an industry survey of 435 senior executives (director level and above) from telcos, network equipment providers, and hyperscalers. All organisations had annual revenue above $1 billion. About 51% of executives were from network; 24% from data/AI and IT; 15% from top management; and 10% from engineering.

The Swiss giant intends to combine its portfolio with open source expertise to expand its managed IT services

Swisscom has become the majority shareholder of Camptocamp, a Swiss developer and integrator of open-source solutions. The operator intends to combines its portfolio with Camptocamp’s open-source expertise to offer IT services that are closely tailored to the needs of Swiss businesses.

The continued development of IT services is a priority for Swisscom. In a rapidly growing market, Swisscom recorded an increase in sales of CHF 32 million (€33.3 million) in its enterprise IT services division last year. Growth came from cloud, security, IoT and applications – and open-source software growing faster than proprietary software.

Geo-info, IoT and ERP

Camptocamp is the market leader in Switzerland in solutions for geo-information systems (GIS), enterprise resource planning (ERP) systems and IT infrastructure management. It is particularly strong in the German-speaking parts of the country.

Thomas Wettstein, Head of IT Solutions Swisscom Business Customers, commented, “Camptocamp complements Swisscom’s already extensive portfolio of solutions, notably in the field of geo-information systems.

“Together, we want to achieve significant growth in this area and bring innovative products and services to the market, particularly in the public sector. This move will ensure that we can provide more tailored support to Swiss companies as they embark on their digital transformation.”

According to Swisscom, managed IT services from trusted sources is becoming particularly important against a backdrop of demands for data sovereignty.

Camptocamp will continue to operate as an independent company and work with its existing customers as usual.

Severina Pascu is appointed Senior Vice President, Commercial and Operations as the group looks for improved share price

Liberty Global has appointed Severina Pascu to the newly created role of Senior Vice President, Commercial and Operations, reporting directly to Liberty Global’s CEO Mike Fries.

Fries is on a mission to shake up Liberty Global’s European businesses, contemplating a range of options to improve its share price which has fallen 5% since the beginning of January.

He said a number of interviews during 2023 that nothing is off the table in his quest to ensure share price reflects the group’s true value. For example, last October, Liberty Global gained 100% ownership of Telenet Group Holding via its wholly-owned subsidiary, Liberty Global Belgium Holding and then delisted the unit from Euronext Brussels.

Last July, Liberty Global announced its shareholders voted in favour of the company changing its jurisdiction of incorporation from England and Wales to Bermuda. The argument for the shift is that it, “incorporation facilitates value-enhancing transactions and reduces administrative burdens and expenses, while preserving strong accountability and corporate governance”.

Last October, Virgin Media O2, Liberty Global’s UK opco agreed to sell a 16.67% minority stake in its mobile tower joint venture, Cornerstone Telecommunications Infrastructure Limited to the UK-based infrastructure fund, GLIL Infrastructure LLP.

In February, the group reported a 1.5% year-on-year drop on a like-for-like basis in annual revenues to almost $7.5 billion (€6.9 billion) for 2023 and an operating loss of $3.87 billion. It made a number of announcements the same month.

Liberty Global will list its shares in Swiss opco Sunrise on the SIX Swiss stock exchange in the second half of 2024 then spin out its entire holding to Liberty Global shareholders.

The group has set up a holding company, Liberty Global Benelux, to manage Telenet’s operations in Belgium and VodafoneZiggo in the Netherlands, in which it has a 50% stake.

Liberty Global is to raise $400 million from its share in the sale of TV production and distribution company All3Media to RedBirdIMI for £1.15 billion.

It announced that subsidiary Telenet was setting up a Network-as-a-Service (NaaS) pilot with Nokia and others at the Port of Antwerp, one of the largest in the world to develop maritime use cases. It has also set up a strategic partnership with AWS to create a NaaS framework.

In short, Pascu is assuming the mantle at a time of great flux for Liberty Global, reporting to a CEO who is in a hurry for results.

She has worked for the group since 2007 in a series of senior roles and brings “operating and commercial expertise in the management of the company’s core FMC [fixed-mobile convergence] champions and venture activities.”

With a cross-functional team, she will be responsible for specific growth and operational improvement programmes in consumer and business segments. The plan is to leverage “scale and excellence across the organization”. There will be no change in the reporting structure of our current operating CEOs at the country level.

Mike Fries, CEO, Liberty Global, commented, “Severina is a world-class operator and leader. Her strong focus on driving change will be instrumental in accelerating the execution of our in-market strategies and shaping our future success. I’m excited to work more closely with her as we implement our value creation strategies across the group.”

Since joining Liberty Global in 2007 as CFO of UPC Romania, Pascu has held positions in many of Liberty Global’s European operations, including helping lead the turnaround of UPC Switzerland as CEO before moving to Virgin Media as CFO and Deputy CEO.

Most recently, she was involved in the merger of Sunrise and UPC Switzerland as Deputy CEO and Chief Commercial Officer for Sunrise.

Prior to joining Liberty Global, Pascu held a number of senior management positions in international companies.

A study by Tefficient reveals some big disparities across Europe’s mobile users from ARPU to revenue per gigabyte

A recent report by consultants Tefficient, commissioned by the Greek regulator the Hellenic Telecommunications & Post Commission (EETT) has highlighted some fascinating insights into mobile services value for money spanning twelve EU and Euro countries: Austria, Belgium, Croatia, France, Germany, Greece, Ireland, Italy, Lithuania, the Netherlands, Slovenia, and Spain.

Tefficient compared key mobile industry metrics, emphasising mobile revenues and data usage, across twelve Eurozone markets within the EU from 2017 to 2023. The analysis derives its insights from actual usage patterns and revenues rather than focussing on the market’s best offerings or theoretical service baskets.

While the primary focus of the benchmark was on Greece, the report’s insights provides perspectives for the telecommunications industry in the remaining eleven countries. Greece has three MNOs, Cosmote, Vodafone, and Nova, but since Vodafone and Nova share mobile network, Greece just has two mobile networks. Within the peer group, only Belgium is in a similar position.

There is no active mobile virtual network operator (MVNO) in Greece. In some of the peer group markets – Germany, Italy, the Netherlands, and Spain – MVNOs hold a 10% or higher market share of mobile subscriptions which suggest that competition stretches well beyond the facilities-based MNOs.

Taking into consideration a range of factors including what statistics were available from each country’s regulator right through to comparative price levels in each country [to show purchasing parity], Ireland topped the ARPU levels at €22.7 but this aligned with it having the highest comparative price level as well. Surprisingly, Croatia featured the second highest ARPU at €17.4 EUR in 1H 2023, despite having the lowest comparative price level.

The ARPU of Greece was 12.2 EUR in 1H 2023 which is lower than the median. The ARPU of Greece was €12.2 in 1H 2023 which is lower than the median while competition in Italy has led to a 5% decline in ARPU. Greece is among the 5 countries (of 11) that had a positive 2017-2022 CAGR in its ARPU. Lithuania has had the best ARPU development at 6%.

Adding in M2M

Croatia topped the charts with €16.4 in 1H 2023 despite its comparative price levels. Ireland had high ARPU levels too, but its fast growth in M2M subscriptions means that the Irish ARPU has fallen quickly. Also Austria has experienced fast growth in its M2M subscriptions base and if including all M2M subscriptions, Austria’s ARPU was the second lowest in 1H 2023, just €7.9. Tefficient pointed out Austria’s numbers were skewed by international SIMs. So with M2M added in, of the twelve countries examined, only two – Lithuania and Greece – had growth in ARPU during 2017-2022.

Mobile data usage per subscription

Tefficient found that Austria had the highest mobile data usage among the peer group. In the first half of 2023, it was 27.1GB per non-M2M subscription per month. Lithuania had the second highest usage, 23.3GB per month in 1H 2023, followed by Croatia with 21.8GB. The usage level of Greece is much lower, 7.3GB per month in the first half of 2023. Until 2020, Greece had the lowest usage among the peer group, but has since overtaken Belgium, Germany, and the Netherlands. All countries have experienced strong growth in the mobile data usage during 2017-2022, but Greece had the fastest growth at 62% – but from a small base.

Data-only drives usage

According to the report, one driver for high average mobile data usage is data-only (or mbb) subscriptions. These SIMs are typically sitting in things like routers, mobile hotspots, PCs or tablets. Austria’s average data-only subscription consumed 115GB per month in the first half of 2023. The overall usage per any subscription was 27.1GB. Lithuania and Ireland also have high average usage per data-only subscription.

Revenue per gigabyte is falling though

Bigger data allowances with stagnant ARPU has meant that revenue per gigabyte has fallen in European countries in the study. The revenue per GB is the highest in Belgium, €3.1 in 2022. Germany had the second highest revenue per GB, €2.8 in 2022. The Netherlands stood at €2.2 in 1H 2023 whereas Greece is fourth-ranked with €1.7 in 1H 2023. In 2019, Greece had the highest revenue per GB, but Greece has fallen below Belgium, Germany, and the Netherlands since. At the other end of the spectrum, Tefficient found Lithuania with just €0.4 per GB in 1H 2023.

Leaner company launches three-year “Free to Run” business strategy which suggests growth will come but so will further cost-cutting

Telecom Italia’s (TIM) board has approved a slate of candidates for its board directorships, with two-thirds of the approved names being new candidates, including business lawyer Alberta Figari for the role of chair, replacing Salvatore Rossi. Current CEO Pietro Labriola has been proposed again to continue the transformation of the telco. Telecom Italia shareholders will vote upon the board renewal on 23 April.

The slimmed down board will comprise nine members, which the company said reflects current practice among various large, listed companies. Existing board member candidates running again are: CEO Pietro Labriola; Giovanni Gorno Tempini; Paola Camagni; Federico Ferro Luzzi; and Maurizio Carli. New candidates include: chair Alberta Figari; Domitilla Benigni; Jeffrey Hedberg; Paola Tagliavini; Romina Guglielmetti; Leone Pattofatto; Antonella Lillo; Andrea Mascetti, Enrico Pazzali, and Luca Rossi.

The telco said its new leaner structure will deliver 8% CAGR core earning over the next three years following the planned sale of its Netco fixed line business. “The sale of the fixed network will allow TIM to move into the market with fewer financial and regulatory constraints,” TIM said in a statement after a board meeting approved a new three-year business plan set out by Labriola. The circa €22 billion Netco deal gives the telco the opportunity to cut debt and costs.

The new business plan, dubbed “Free to Run” also includes a revenue target of 3% CAGR. According to Reuters, the telco reported revenue of €14.4bn, on a proforma basis, for the new structure last year, while EBITDA including lease costs stood at €3.5bn on the same basis.

Domestic growth

For its domestic business, TIM forecast a growth of core earnings at an annual rate of 9-10% over the period on a compound basis, from €1.9bn euros last year. The business plan suggests that TIM’s domestic consumer business would stabilise its revenue base by building up partnerships to sell its customers a wide range of services beyond connectivity, according to Reuter, while the enterprise arm would continue its growth helped by an expanding cloud market.

The telco said it expects to generate positive free cash flow both in Italy and from its Brazil-listed unit in the period to 2026. The telco also expects its debt after lease to fall to 1.6-1.7 times its core earnings in 2026, from 3.8 times last year under the current structure, once the Netco deal is completed in the middle of this year.

Cutting more costs

Last week, TIM’s management opened negotiations with unions to reduce working hours for many of its Italian-based employees – with the alternative being potential job cuts if no agreement is reached. Management pointed the finger at the government ending a funded scheme linked to training programmes. TIM is reportedly seeking a 10-20% reduction in working hours until 30 June 2025 for almost 36,000 workers – with a similar reduction in pay.

This week the towerco reported a 16% rise in annual revenues to €4 billion and ended the year with €20bn debt

Cellnex is to sell its unit in Ireland to Phoenix Tower International (PTI) for €971 million.

Cellnex’s CEO, Marco Patuano, commented in a statement that the sale “is one further step within the company’s ‘Next Chapter’, in line with our strategy, to achieve the goal of consolidating, simplifying our corporate structure and focusing our efforts in the existing growth opportunities in the main markets in which we operate.”

Last week Cellnex reported a 16% rise in annual revenues to €4 billion and ended the financial year with €20.1 billion net debt. At its Capital Markets Day yesterday, it reiterated its commitment to attaining investment-grade rating from S&P and becoming a leading neutral infrastructure provider in Europe.

More deals are expected. Cellnex has just completed the sale of its private networks business, most Edzcom, to Boldyn Networks. The financial details have not been made public.

It also sold a minority shareholding of 49% for its businesses in Sweden and Denmark to Stonepeak for €730 million last September.

PTI gains ground

Dagan Kasavana, CEO of PTIadded, “We are delighted to announce this strategic transaction with Cellnex after a successful transaction in France* which signifies a significant step forward in Phoenix Tower International’s expansion in Europe.

“This acquisition demonstrates our commitment to Ireland, and we are eager to contribute to the development of robust and advanced telecommunications infrastructure that will benefit both the Irish people and our valued mobile network operator partners. We appreciated the Cellnex team’s constructive approach and hard work to sign this transaction.”

* Cellnex was obliged to sell 2,353 sites in France to PTI and Bouygues Telecom last year was part of the remedies put in place by the French Competition Authority (FCA) after Cellnex acquired Hivory in 2021. This brought Cellnex €631 million. The sale of another 870 sites should go ahead this year raising an additional €360 million.

Consolidation in test and measurement market after grim 2023, partly bankrolled by private investment in public equity via Silver Lake

The US’ Viavi Solutionsintends to acquire the UK’s Spirent Communications for £1 billion (€1.17 billion). The announcement caused Spirent’s shares to rise by 62%, reaching levels not seen since last summer.

The news came as Spirent announced its annual financial results for 2023 which showed a 22% drop in revenues to $474.3 million (€437 million compared with the previous year. Adjusted operating profit fell by 65.1% to $45.2 million.

Spirent’s CEO Eric Updyke commented: “As we progressed through 2023, the market landscape became increasingly challenging. The elevated prevailing interest rates and inflationary pressures impacted customers, especially those in the telecommunications sector.

“These customers responded by taking significant action, particularly in the second half of 2023, to cut costs and by reducing their capital expenditure to preserve cash.”

He pointed out that Spirent has signed new 5G and Open RAN contracts, and looked to expand its business outside the telecoms sector, for example securing an important deal in financial services and ongoing success with hyperscaler customers.

Oleg Khaykin, President and CEO of Viavi, noted, “Combining our leading communications test and measurement and optical technologies and Spirent’s high-performance testing and assurance solutions is expected to deliver enhanced product solutions and applications, accelerate growth in new markets and strengthen innovation through expanded engineering and design capabilities.”

British firms are cheap

The companies said in a statement, “Spirent’s product offerings and technological assets are highly complementary and synergistic to Viavi’s existing portfolio, which will enable the Combined Group to deliver high performance, integrated solutions for networking and mission critical applications, including 5G and 6G wireless infrastructure.”

The deal is attractive as now both companies gain exposure to each other’s customer base and there is project reduction of $75 million in operating costs. As the Financial Times [subscription needed] pointed out, this is about half of Spirent’s 2023 earnings beforeinterest, taxes, depreciation, and amortisation (EBIDTA).

The acquisition will be funded by cash Viavi holds, an $800m seven-year term loan from Wells Fargo Bank, and a $400m investment from Silver Lake in the form of a convertible note. Ken Hao, Chairman and Managing Partner of Silver Lake, will join the Viavi board of directors.

PIPE might become more common

The deal is also interesting because it will be financed in part by a $400 million convertible loan from private equity firm Silver Lake. Such deals are known as private investments in public equity (PIPE) and relatively common in the US.

Private equity firms are insulated from a deal going wrong while gaining a route into a company’s share capital. Silver Lake eventually acquired Germany’s Software AG but started in the same way as the Spirent deal is structured.

Viavi would have found it difficult to fund the deal with straight debt as it too is experiencing tough times due to market conditions, with its projected 2024 EBIDTA expected to be $165 million, compared with from $260 million in 2022.